{kind=link}

Many moons ago my own particular choice was to turn down a partnership at a perfectly respectable large firm and strike out on my own. In a pre-cloud world this required significant investments in infrastructure and ‘locked-in’ desktop software arrangements; even so, it was a decision that I never regretted.

Key to establishing my successful firm was getting crystal clear on why I was making this leap into the unknown, and what I wanted the firm to do. Without this understanding, it would have been so easy to fall back on traditional expectations and to ultimately end up as yet another compliance hen-house.

Identifying the Why?

One of the most popular TedX videos is Simon Sinek’s inspiring presentation from 2009. If you are one of the few that hasn’t been exposed to this talk, make sure that you are soon.

The Sinek video neatly captures the importance of “why?” in business. It also starkly challenges us too, with the killer question,: “why do you get out of bed in the morning – and why should anyone care?”

These are powerful, personal questions and I believe this is where your value-add journey must start. Without a North Star, the journey will be that much harder to successfully navigate.

Simon Sinek’s “why?” challenge always takes me back to the younger me of twenty years ago, blinking in the surprise and shock of my first week in an accounting practice. When that first shoebox of receipts slid across my desk, when I was first made aware that we had urgent deadlines and grumpy clients, I realised that my existential “why?” was out of sync with my career choice.

Thankfully, I suspected that there had to be more. There had to be a purpose beyond number-crunching.

I eventually found my purpose in the discovery and provision of services that add value for clients, that have the power to surprise and delight – and that can actually change lives. Yes, accountants can change lives too.

Our expertise and experience can be used for more, much more, than historic, rear-view accounting. But I knew this was a minority view in a traditional accounting firm, where reactive and regulated service provision was the order of the day. It was time to start afresh.

Start Me Up

Identifying your North Star is one thing – aiming your rocket-ship and reaching your destination is quite another. Getting off the launch pad and punching through the atmosphere at the right velocity without over-heating or breaking up is the really tricky part.

It can be lonely and just a bit scary starting a new venture. Selling a different vision to a market where low expectations and customer apathy are endemic can be hard work.

Luckily, it’s easier now than it was even a decade or so ago. In fact, I believe that there is no better time to create your own accounting practice than the present.

Long gone are the days of big servers, clunky software and mortgaging your house to get fuel in the tank. Cloud technology – it’s sheer simplicity and accessibility has changed all of that.

The cloud has not only broken down barriers to entry (cost and infrastructure) but also opened up opportunity (ease of market reach and online collaboration) for seedling firms. Start and stay on the cloud.

I think the market is also waking up to the possibility and desirability of entrepreneur-accountants. These accountants think like other business owners and really care about their success. Is this you?

So what better environment in which to start the engines and get going?

Designing the Future

The tough choices you have to make are all about your business ‘design’. Designing a fit-for-the-future business is easier now thanks to the path-finder firms of the last few years who can be emulated, but your design still has to resonate with you and link back to your personal ‘why?’

When I designed my boutique, value-add consultancy I decided to do 2 things:

- Make a bold statement of intent; and

- Put in place some ‘building blocks’ that would stand the test of time.

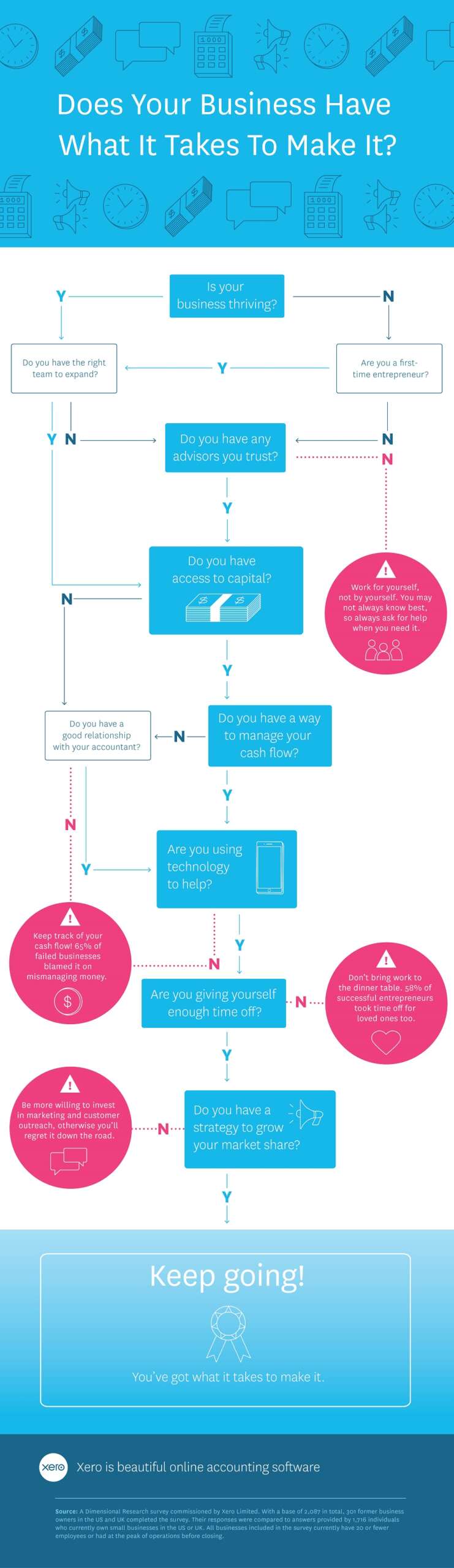

My statement of intent is summed up in this diagram I drew:

Now, this alone was scary stuff – accounting sacrilege, even. Essentially, my accounting firm was to be wholly inverted from the norm, where 80% compliance fee reliance is typical. I was committing to going to a place where few had gone or were prepared to go; 80% value-add.

So how to get there?

This is where my building blocks come in; the essential design elements for my value-add consultancy. I share them below:

These building blocks were laid around the client as central hub, as you’ll see. The client is not only at the centre, but defined; in my case by a desire to work with growing, ambitious technology and/or creative businesses.

I wanted rewarding, proactive and collaborative work on a scale I could manage. This meant I could grow a small, close-knit team and a modest client-base of interesting and aspirational clients.

In building our business model, we weren’t fixated on a specialism or market niche per se. We did, however, gravitate to the energy and excitement of Wellington’s emerging web and tech scene.

I wanted to work with edgy start-ups, entrepreneurs and aspirational folk that were moving the needle. These businesses would, almost by definition, need Virtual CFO and trusted advisor input.

We therefore designed our services to add maximum value and to ‘make sense’ to our market demographic. I’ll discuss this more later, but our model was to be a Virtual CFO firm that happened to do a spot of accounting.

Connecting and selling to these businesses was an urgent and important consideration. I had no existing clients, so there was nothing like rent and wage payments looming to get me out and about into the thick of the market.

Now, much ink has been spent on how accountants are poor at selling and getting themselves in front of new customers; this is at least partly true, but also a generalisation. Good people will find the way to convey the right messages, listen to the customer and then devise a joint plan of attack. If this is a struggle, get some expert help.

My own focus was to find my target market at incubators, accelerators and to do online research. Who were the best start-ups, most ambitious businesses in the local tech and creative sectors?

I especially wanted to move beyond the traditional “do they have a wallet and a heart-beat?” approach to accounting client acceptance. We had to have gating criteria and be prepared to say “no” – and even to exit clients that we had accepted for the wrong reasons.

I identified and connected with these businesses personally – relying on adverts, sponsorships and trade shows is a tired and generic approach (I know, I tried these too). I provided services, seminars and initial advice (sometimes for free or heavily discounted) until I was in a position to package up the right menu of services, heavily aligned with the client’s own expectations of growth, success and achievement.

Whilst I had a menu of services, I deliberately didn’t have a ‘one easy fee’ McHappy Meal approach to customer pricing and packages. This may suit some customer types, particularly at the micro end of town, but it’s an approach that can, I feel, restrict the vision and ambition of both accountant and client.

Once a steady hum of advisory and accounting work had been explicitly agreed with customers, I left lots of leeway and expectation for special projects and extensions to the core offering. This was essential for growing ARPU (Average Revenue Per Client) and, perhaps counter-intuitively, customer satisfaction.

(I’ll talk more about growing value-add ARPU and client satisfaction concurrently in a future post).

Virtual CFO

For me to deliver on my promise and their expectation levels, it made perfect sense to position as their Virtual CFO. By aligning my expertise and disposition (I love trends, insight and analysis) with their desire to learn, explore and grow, it was a perfect fit.

Being the Virtual CFO opened up other value-add service offerings, underpinned by the rigour of monthly Spotlight Reports (then done as simplistic one-pagers in EXCEL!), advisory meetings and action plans. We set KPI’s and monitored them, we set the Strategy and looked at scenarios. We mentored the business owners to a regular and agreed schedule, and helped them through all of the usual growth business pain points.

Being able to anchor my service provision around the ‘low hanging fruit’ of data analysis, reporting and forecasting was quite simply pivotal to our success. The steady injection of monthly advanced reporting and insight matured so that the client enquiry of “where’s my Spotlight?” became the norm.

Of course, the accounting and tax work followed – often from aggrieved traditional firms who had never twigged to the fact that I (another CA, no less!) was actually already doing all of the higher-value, fun stuff. Happy days.

As our consultancy grew, we knew we needed to collaborate with others and share the journey. Getting other trusted advisors involved – even other accountants – for roles on Advisory Boards, as industry experts or for skill-gap filling like lawyers or HR people, was also an important step. We became facilitators.

Growing a brand was an important building block initially, but as I had come to the decision that my firm would be a ‘consultancy’ of boutique size and positioning, I could personalise the brand and develop this organically. Because I wasn’t trying to grow the funnel size at all costs, I could focus on distilling the value from and for existing clients and collaborators.

Personal time and the work/life balance ethos were critical to this decision, so we needed to be smart and grow depth rather than volume. I had no desire to be the biggest cheese on the cheese-board, which was a very liberating position to operate from.

One year we even exited 10 clients and passed on tens of thousands of dollars worth of fees. Why? We had started to stray from our purpose and the client criteria we had set for ourselves, impacting not only morale but also the quality and enjoyment of what we were doing.

This cull was one of the best things we ever did. We were actively designing our future by ensuring that clients were moved on to firms that were a better fit for them and us.

Hiring in the right mix of skills for a value-add consultancy was the toughest nut to crack. As we expected to be in front of our clients at least every month, if not every week, we needed to blend account management, solution-providing and professional discipline to all that we did. Finding this mix in the employment market can be tough but ultimately your team must have as much ‘can do’ attitude as technical skill.

Lastly, but by no means least, your tool-set needs to be relevant, robust and scalable. In desk-top days, this was hard yards, but it did lead me to create some useful and popular prototypes for Spotlight Reporting as a foundation tool for client discourse.

Xero, of course, changed the game. The brainchild of Rod Drury and Hamish Edwards was a visionary spin on core accounting, and it was an easy decision for us to partner with Xero right back in its start-up days.

Our early adoption of cloud tools like Xero – and then the creation of our own online Spotlight Reporting suite of apps – simplified and improved our delivery mechanism. Easy, accessible and collaborative – game on.

After many years of delivering value-add services successfully, the seeds of a new journey were planted. Soon I was to morph from Trusted Advisor and founder of the first independent Xero Partner firm to CEO of a creative, technology company of my own – Spotlight Reporting, now the most popular reporting application in the Xero eco-system. But that’s another story.

Building a value-add consultancy from the ground up was a lot of hard work, but extremely challenging and rewarding too. Your own building blocks will, I’m sure, be a bit different. But I encourage you to grab some whiteboard markers, a trusted collaborator or two, and start drawing the future.

{kind=link}

{kind=link}

{kind=link}